---

title: "Multiple Linear Regression in R: A Practical Guide"

format:

html:

toc: true

code-fold: true

number-sections: true

execute:

echo: true

warning: false

message: false

editor:

markdown:

wrap: 72

---

# Introduction

This notebook is a practical refresher on multiple linear regression in

R. It is written for someone who already knows the broad idea of

regression, but wants a clear reference for the workflow: how to set up

the data, fit the model, check the assumptions, and interpret the

output without hand-waving.

The example uses systolic blood pressure (SBP) from NHANES 2021–2023.

The aim is not to turn this into a textbook chapter. The aim is to keep

the useful theory close to the code and the modelling decisions, so the

notebook is something you can come back to when you need to get up to

speed quickly.

The main question is straightforward: can we explain variation in SBP

using demographics, social determinants of health, and lifestyle

factors in the same model?

## Where MLR Fits: The GLM Family

Multiple linear regression sits inside the **Generalised Linear Model

(GLM)** family. The main reason to mention that here is practical: it

helps explain why linear, logistic, and Poisson regression feel similar

in R even though they handle different outcome types.

| Model | Outcome type | Distribution | Link function | Coefficient interpretation |

|---|---|---|---|---|

| **Linear regression** | Continuous | Gaussian | Identity | Change in $Y$ per unit change in $X$ |

| **Logistic regression** | Binary (0/1) | Binomial | Logit | Change in log-odds per unit change in $X$ |

| **Poisson regression** | Count | Poisson | Log | Change in log-rate per unit change in $X$ |

In linear regression, the **identity link** means the model works

directly on the outcome scale. Logistic regression uses the **logit

link** because probabilities are bounded between 0 and 1, and Poisson

regression uses the **log link** because counts are non-negative. The

core setup is the same; the outcome distribution and link function are

what change.

::: {.callout-note title="Why does the link function matter?" collapse="true"}

Linear regression assumes the outcome is continuous and unbounded. A

raw probability, however, is bounded between 0 and 1 — so you cannot

directly model it as a linear function of predictors without risking

predicted values outside that range.

The logit link solves this:

$$\log\left(\frac{p}{1-p}\right) = \beta_0 + \beta_1 X_1 + \cdots + \beta_p X_p$$

The left-hand side (log-odds) is unbounded, so a linear predictor on

the right is appropriate. The cost is that coefficients are now in

log-odds units, which are less intuitive to interpret — hence the common

practice of exponentiating them to obtain **odds ratios**.

In linear regression, no such transformation is needed. The identity

link means:

$$E[Y] = \beta_0 + \beta_1 X_1 + \cdots + \beta_p X_p$$

Coefficients are directly interpretable as changes in $Y$.

:::

## The Research Question

This analysis asks: **how much of the variation in systolic blood

pressure can be explained by social and lifestyle factors beyond age,

sex, and race?**

To answer that, we fit two nested models:

- **Base model:** SBP ~ age + sex + race

- **Full model:** SBP ~ age + sex + race + education + poverty ratio +

food security + physical activity + sedentary time + sleep + smoking +

waist circumference + diabetes

---

# Setup and Data Import

## Packages

The package set is small and standard. Nothing here is unusual for an R

regression workflow.

```{r}

#| label: setup

library(here) # Reproducible file paths

library(tidyverse) # Data wrangling and visualisation

library(arrow) # Reading parquet files

library(broom) # Tidying model output

library(patchwork) # Combining plots

library(car) # VIF and diagnostic tests

```

::: {.callout-tip title="Why These Packages?" collapse="true"}

**`here`**

Constructs file paths relative to the project root, so code runs

regardless of where the working directory is set. Essential for

reproducibility. Alternative: `rprojroot`, or simply using absolute

paths (fragile and not portable).

**`tidyverse`**

A collection of packages sharing a common design philosophy. The core

packages used here are:

- `dplyr` — data manipulation (`mutate()`, `filter()`, `select()`)

- `tidyr` — reshaping data (`pivot_longer()`, `drop_na()`)

- `ggplot2` — layered graphics

- `stringr` — string manipulation

- `forcats` — factor handling

Alternative for wrangling: `data.table` (much faster for large

datasets, but with a steeper syntax). For plotting, base R graphics or

`lattice` are alternatives, though `ggplot2` is now the de facto

standard.

**`arrow`**

Reads and writes Apache Parquet files — a columnar storage format that

is compact and fast to read, especially for large datasets. Alternative:

`readr` for CSV, `haven` for Stata/SPSS/SAS files.

**`broom`**

Converts model objects (like `lm`) into tidy data frames. The key

functions are:

- `tidy()` — coefficient table with estimates, SEs, t-statistics,

p-values

- `glance()` — model-level summary (R², F-statistic, AIC, etc.)

- `augment()` — adds fitted values and residuals back to the original

data

Without `broom`, you would extract these manually from `summary(model)`

— which works but is messier.

**`patchwork`**

Combines multiple `ggplot2` objects into a single figure using intuitive

syntax (`p1 | p2` for side-by-side, `p1 / p2` for stacked). Alternative:

`gridExtra::grid.arrange()`.

**`car`**

The *Companion to Applied Regression* package. Used here for:

- `vif()` — variance inflation factors (collinearity diagnostics)

- `ncvTest()` — Breusch-Pagan test for non-constant variance

Alternative for VIF: `performance::check_collinearity()` from the

`performance` package. For the Breusch-Pagan test: `lmtest::bptest()`.

:::

## Data Import and Wrangling

The wrangling pipeline matches the other notebooks in this project. The

main jobs are to clean NHANES sentinel values, derive the physical

activity variable, recode the categorical predictors, and restrict the

analysis to complete cases for the variables used in the model.

```{r}

#| label: import

source(here("R", "plot_theme.R"))

df_raw <- read_parquet(here("data", "processed", "analysis_dataset.parquet"))

df <- df_raw |>

mutate(

mod_min_session = if_else(mod_min_session %in% c(7777, 9999), NA_real_, mod_min_session),

vig_min_session = if_else(vig_min_session %in% c(7777, 9999), NA_real_, vig_min_session),

vig_freq = if_else(vig_freq %in% c(7777, 9999), NA_real_, vig_freq),

sedentary_min_day = if_else(sedentary_min_day %in% c(7777, 9999), NA_real_, sedentary_min_day),

mod_freq_per_week = case_when(

mod_freq_unit == "D" ~ mod_freq * 7,

mod_freq_unit == "W" ~ mod_freq,

mod_freq_unit == "M" ~ mod_freq / 4.3,

mod_freq_unit == "Y" ~ mod_freq / 52,

TRUE ~ NA_real_

),

vig_freq_per_week = case_when(

vig_freq_unit == "D" ~ vig_freq * 7,

vig_freq_unit == "W" ~ vig_freq,

vig_freq_unit == "M" ~ vig_freq / 4.3,

vig_freq_unit == "Y" ~ vig_freq / 52,

TRUE ~ NA_real_

),

mod_met = coalesce(mod_freq_per_week * mod_min_session, 0) * 4,

vig_met = coalesce(vig_freq_per_week * vig_min_session, 0) * 8,

total_met = mod_met + vig_met,

log_total_met = log(total_met + 1)

) |>

mutate(

sex = factor(

case_when(sex_raw == 1 ~ "Male", sex_raw == 2 ~ "Female"),

levels = c("Male", "Female")

),

race = factor(

case_when(

race_raw == 1 ~ "Mexican American",

race_raw == 2 ~ "Other Hispanic",

race_raw == 3 ~ "Non-Hispanic White",

race_raw == 4 ~ "Non-Hispanic Black",

race_raw == 6 ~ "Non-Hispanic Asian",

race_raw == 7 ~ "Other/Multiracial"

),

levels = c(

"Non-Hispanic White", "Mexican American", "Other Hispanic",

"Non-Hispanic Black", "Non-Hispanic Asian", "Other/Multiracial"

)

),

education = factor(

case_when(

education_raw == 1 ~ "Less than 9th grade",

education_raw == 2 ~ "9th-11th grade",

education_raw == 3 ~ "High school grad / GED",

education_raw == 4 ~ "Some college / AA degree",

education_raw == 5 ~ "College graduate or above",

education_raw %in% c(7, 9) ~ NA_character_

),

levels = c(

"College graduate or above", "Some college / AA degree",

"High school grad / GED", "9th-11th grade", "Less than 9th grade"

)

),

smoking_status = factor(

case_when(

ever_smoked == 2 ~ "Never",

ever_smoked == 1 & current_smoker == 3 ~ "Former",

ever_smoked == 1 & current_smoker %in% c(1, 2) ~ "Current",

TRUE ~ NA_character_

),

levels = c("Never", "Former", "Current")

),

food_security = factor(

case_when(

food_security_raw == 1 ~ "Fully food secure",

food_security_raw == 2 ~ "Marginally food secure",

food_security_raw == 3 ~ "Low food security",

food_security_raw == 4 ~ "Very low food security"

),

levels = c(

"Fully food secure", "Marginally food secure",

"Low food security", "Very low food security"

)

),

diabetes_flag = factor(

case_when(

diabetes_diagnosis == 1 ~ "Yes",

diabetes_diagnosis %in% c(2, 3) ~ "No",

diabetes_diagnosis %in% c(7, 9) ~ NA_character_

),

levels = c("No", "Yes")

),

poverty_ratio = poverty_raw

)

model_vars <- c(

"sbp", "log_total_met", "sedentary_min_day", "age", "sex", "race",

"education", "waist_cm", "poverty_ratio", "sleep_hours", "smoking_status",

"food_security", "diabetes_flag"

)

df_cc <- df |>

drop_na(all_of(model_vars)) |>

select(id, all_of(model_vars), mec_weight, psu, strata)

```

::: {.callout-note title="Why use complete cases?" collapse="true"}

`drop_na(all_of(model_vars))` gives a **complete case analysis (CCA)**:

only participants with non-missing values on every modelling variable

are retained.

That is a pragmatic choice rather than an ideal one. CCA is simplest to

explain and keeps the modelling workflow easy to follow, but it assumes

the excluded records are not introducing serious bias. If missingness

looked more systematic, multiple imputation would be the better next

step.

For this notebook, the tradeoff is acceptable because the complete case

sample ($n =$ `r nrow(df_cc)`) is still large and the goal is to

document the regression workflow clearly.

:::

## Variable Summary

| Variable | Type | Role | Notes |

|---|---|---|---|

| `sbp` | Continuous | Outcome | Systolic blood pressure (mmHg) |

| `age` | Continuous | Predictor | Age in years |

| `sex` | Categorical (2 levels) | Predictor | Reference: Male |

| `race` | Categorical (6 levels) | Predictor | Reference: Non-Hispanic White |

| `education` | Ordinal (5 levels) | Predictor | Reference: College graduate or above |

| `poverty_ratio` | Continuous | Predictor | Income-to-poverty ratio |

| `food_security` | Ordinal (4 levels) | Predictor | Reference: Fully food secure |

| `log_total_met` | Continuous (log-transformed) | Predictor | Physical activity in MET-min/week |

| `sedentary_min_day` | Continuous | Predictor | Sedentary time (min/day) |

| `sleep_hours` | Continuous | Predictor | Self-reported sleep hours/night |

| `smoking_status` | Categorical (3 levels) | Predictor | Reference: Never smoker |

| `waist_cm` | Continuous | Predictor | Waist circumference (cm) |

| `diabetes_flag` | Categorical (2 levels) | Predictor | Reference: No diabetes |

---

# Exploratory Analysis

Before fitting any model, we check the parts of the data that will

drive modelling decisions: the outcome distribution, the shape of the

continuous predictor relationships, and the degree of overlap between

predictors.

## Outcome Distribution

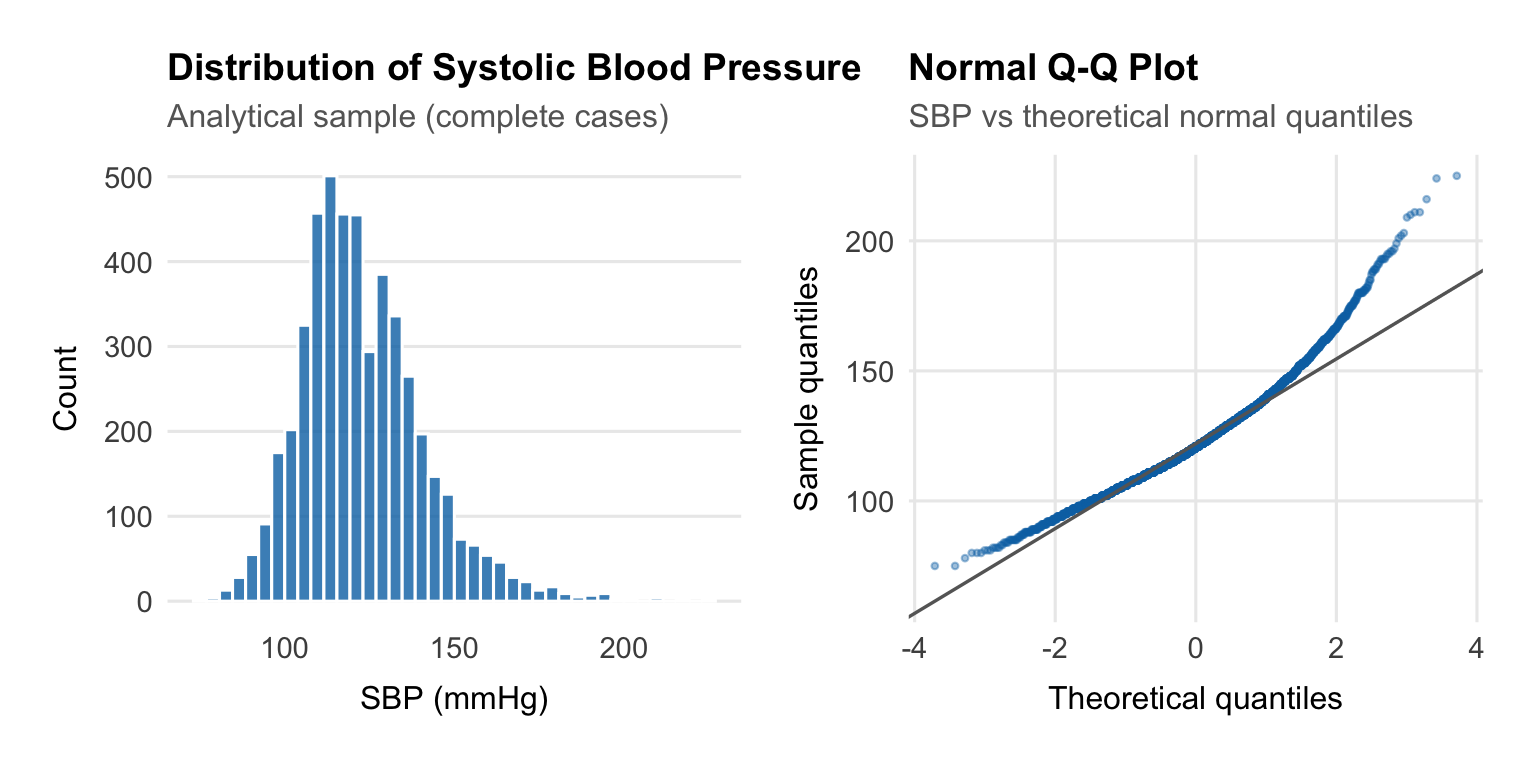

We begin by examining SBP, the outcome variable.

```{r}

#| label: fig-sbp-dist

#| fig-width: 8

#| fig-height: 4

p_hist <- ggplot(df_cc, aes(x = sbp)) +

geom_histogram(bins = 40, fill = palette_epi[["blue"]], alpha = 0.8, colour = "white") +

labs(

title = "Distribution of Systolic Blood Pressure",

subtitle = "Analytical sample (complete cases)",

x = "SBP (mmHg)",

y = "Count"

) +

theme_epi(grid = "y")

p_qq <- ggplot(df_cc, aes(sample = sbp)) +

stat_qq(colour = palette_epi[["blue"]], alpha = 0.4, size = 0.8) +

stat_qq_line(colour = "grey40", linewidth = 0.6) +

labs(

title = "Normal Q-Q Plot",

subtitle = "SBP vs theoretical normal quantiles",

x = "Theoretical quantiles",

y = "Sample quantiles"

) +

theme_epi(grid = "both")

p_hist | p_qq

```

Linear regression cares about the **residuals**, not the raw outcome,

but it is still useful to check the outcome first. Here SBP is roughly

symmetric with a mild right tail from higher readings. That is typical

for blood pressure data and does not justify transforming the outcome.

::: {.callout-note title="Does the outcome need to be normally distributed?" collapse="true"}

A common misconception is that MLR requires the outcome variable to be

normally distributed. This is not quite right.

The formal assumption is that the **errors** $\varepsilon_i \sim N(0,

\sigma^2)$ — not the raw outcome. If the model is correctly specified

(the right predictors, the right functional form), the residuals should

be approximately normal even if the raw outcome is mildly skewed.

That said, a severely skewed outcome — for example, a strongly

right-skewed cost variable with a spike at zero — often does produce

non-normal residuals. In such cases, a **log transformation** of the

outcome is common. This changes the interpretation: coefficients then

describe multiplicative rather than additive effects.

For SBP, the distribution is close enough to symmetric that

transformation is not necessary.

:::

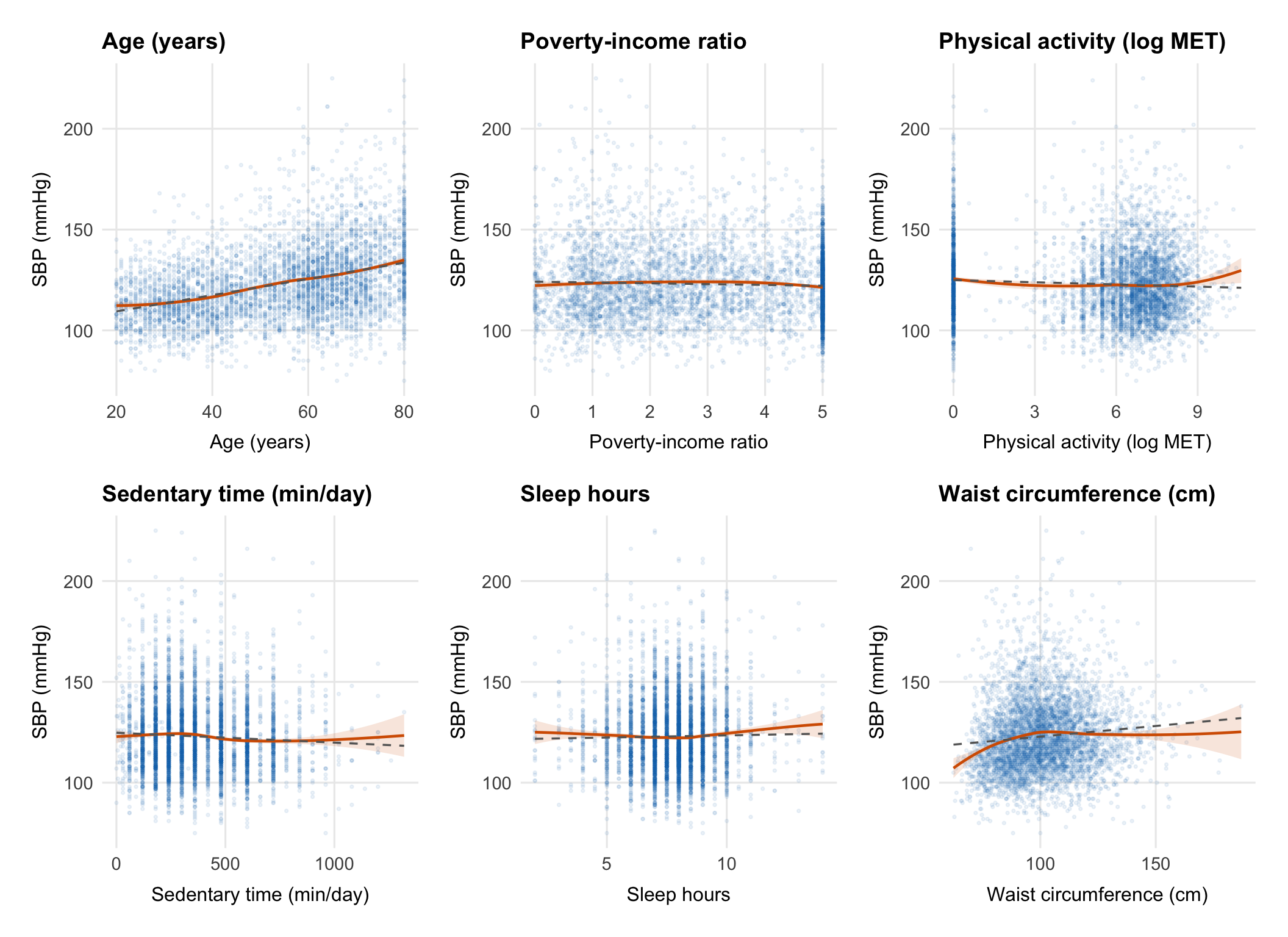

## Linearity Checks

The main question here is whether the continuous predictors look roughly

linear on the SBP scale or whether any of them need a transformation or

more flexible term before we fit the model.

```{r}

#| label: fig-linearity

#| fig-width: 11

#| fig-height: 8

continuous_vars <- c("age", "poverty_ratio", "log_total_met",

"sedentary_min_day", "sleep_hours", "waist_cm")

var_labels <- c(

age = "Age (years)",

poverty_ratio = "Poverty-income ratio",

log_total_met = "Physical activity (log MET)",

sedentary_min_day = "Sedentary time (min/day)",

sleep_hours = "Sleep hours",

waist_cm = "Waist circumference (cm)"

)

plots <- map(continuous_vars, function(var) {

ggplot(df_cc, aes(x = .data[[var]], y = sbp)) +

geom_point(alpha = 0.08, size = 0.6, colour = palette_epi[["blue"]]) +

geom_smooth(method = "loess", se = TRUE, colour = palette_epi[["vermillion"]],

linewidth = 0.8, fill = palette_epi[["vermillion"]], alpha = 0.15) +

geom_smooth(method = "lm", se = FALSE, colour = "grey40",

linewidth = 0.6, linetype = "dashed") +

labs(

title = var_labels[var],

x = var_labels[var],

y = "SBP (mmHg)"

) +

theme_epi(grid = "both")

})

wrap_plots(plots, ncol = 3)

```

Each panel compares a LOESS smooth (red) with a straight-line fit

(dashed grey). If they track closely, a linear term is probably fine.

If they diverge, that predictor may need a transformation or spline.

::: {.callout-note title="What is LOESS and why use it here?" collapse="true"}

**LOESS** (Locally Estimated Scatterplot Smoothing) is a

non-parametric smoother that fits a local regression at each point in

the data using a weighted neighbourhood of observations. It makes no

assumption about the global shape of the relationship — it simply lets

the data speak.

This makes it ideal for checking whether the assumption of linearity is

reasonable. If the LOESS curve is approximately straight, a linear term

is defensible. If it curves meaningfully, you have options:

- **Log-transform the predictor** (useful for right-skewed predictors

with a decelerating relationship)

- **Add a polynomial term** (e.g., $X + X^2$ for a quadratic

relationship)

- **Use a spline** (e.g., `ns(X, df = 3)` for a flexible smooth curve

that doesn't assume any specific shape)

The physical activity predictor (`total_met`) is already

log-transformed here because the raw MET distribution is extremely

right-skewed and the relationship with SBP is approximately

log-linear.

:::

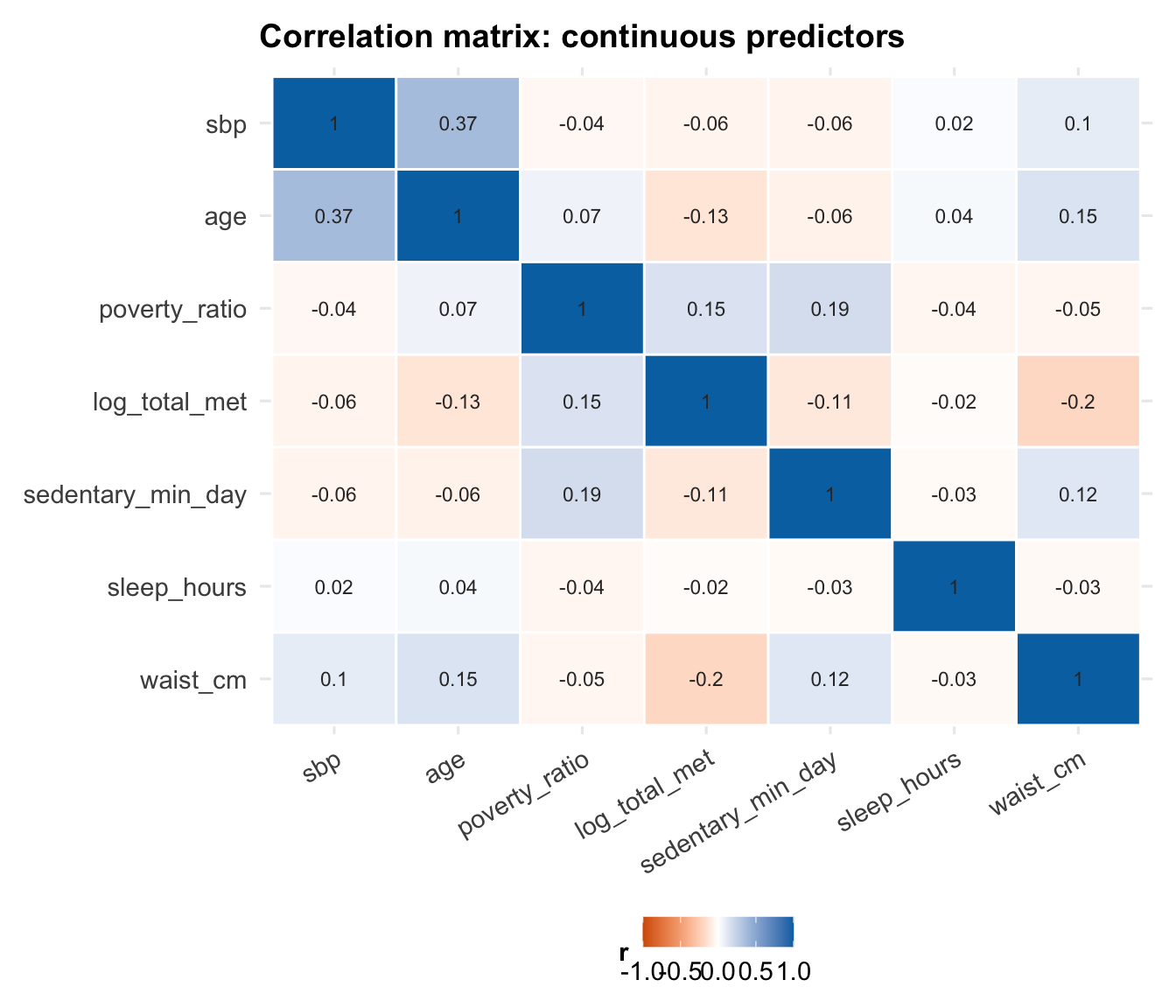

## Collinearity

Before fitting the model, it is also worth checking whether any

continuous predictors are so correlated that they are likely to cause

interpretation or stability problems later.

```{r}

#| label: fig-correlation

#| fig-width: 7

#| fig-height: 6

cor_data <- df_cc |>

select(sbp, age, poverty_ratio, log_total_met,

sedentary_min_day, sleep_hours, waist_cm) |>

cor(use = "complete.obs")

cor_data |>

as.data.frame() |>

rownames_to_column("var1") |>

pivot_longer(-var1, names_to = "var2", values_to = "r") |>

mutate(

var1 = factor(var1, levels = colnames(cor_data)),

var2 = factor(var2, levels = rev(colnames(cor_data)))

) |>

ggplot(aes(x = var1, y = var2, fill = r)) +

geom_tile(colour = "white", linewidth = 0.5) +

geom_text(aes(label = round(r, 2)), size = 3, colour = "grey20") +

scale_fill_gradient2(

low = palette_epi[["vermillion"]],

mid = "white",

high = palette_epi[["blue"]],

midpoint = 0,

limits = c(-1, 1)

) +

labs(

title = "Correlation matrix: continuous predictors",

x = NULL,

y = NULL,

fill = "r"

) +

theme_epi() +

theme(axis.text.x = element_text(angle = 30, hjust = 1))

```

::: {.callout-note title="What is collinearity and why does it matter?" collapse="true"}

**Collinearity** (or multicollinearity) occurs when two or more

predictors in a regression model are highly correlated with each other.

This matters because MLR estimates the effect of each predictor

**holding all others constant**. When two predictors move together,

there is little independent variation in each to work with. The model

struggles to distinguish their separate effects, and the result is:

- **Inflated standard errors** — the confidence intervals on

coefficients widen substantially

- **Unstable estimates** — small changes in the data can cause large

swings in the estimated coefficients

- **Difficult interpretation** — the coefficient for $X_1$ represents

its effect "holding $X_2$ constant", but if $X_1$ and $X_2$ almost

always move together in the real world, this conditional effect is

rarely observed

Collinearity does **not** bias coefficient estimates — it just makes

them imprecise. It also does not affect the model's predictive

performance if future data come from the same distribution.

We quantify collinearity after fitting the model using **Variance

Inflation Factors (VIFs)** — see the diagnostics section.

:::

---

# The Multiple Linear Regression Model

This section keeps the theory that is most useful when reading model

output. The goal is not to reproduce a full regression lecture, but to

keep the key ideas close to the analysis.

## The Model Equation

In multiple linear regression, we model the expected value of a

continuous outcome $Y$ as a linear function of $p$ predictors:

$$Y_i = \beta_0 + \beta_1 X_{i1} + \beta_2 X_{i2} + \cdots + \beta_p X_{ip} + \varepsilon_i$$

where:

- $Y_i$ is the observed outcome for subject $i$ (SBP in mmHg)

- $\beta_0$ is the **intercept** — the expected value of $Y$ when all

predictors equal zero

- $\beta_j$ is the **partial regression coefficient** for predictor $j$

— the expected change in $Y$ for a one-unit increase in $X_j$, **holding

all other predictors constant**

- $\varepsilon_i$ is the **error term** — the part of $Y_i$ not

explained by the predictors

The errors are assumed to be independent and identically distributed:

$\varepsilon_i \overset{iid}{\sim} N(0, \sigma^2)$.

## Matrix Form

For $n$ observations and $p$ predictors, the model is written compactly

in matrix form:

$$\mathbf{Y} = \mathbf{X}\boldsymbol{\beta} + \boldsymbol{\varepsilon}$$

where:

$$\mathbf{Y} = \begin{pmatrix} Y_1 \\ Y_2 \\ \vdots \\ Y_n \end{pmatrix}, \quad

\mathbf{X} = \begin{pmatrix} 1 & X_{11} & \cdots & X_{1p} \\ 1 & X_{21} & \cdots & X_{2p} \\ \vdots & \vdots & \ddots & \vdots \\ 1 & X_{n1} & \cdots & X_{np} \end{pmatrix}, \quad

\boldsymbol{\beta} = \begin{pmatrix} \beta_0 \\ \beta_1 \\ \vdots \\ \beta_p \end{pmatrix}, \quad

\boldsymbol{\varepsilon} = \begin{pmatrix} \varepsilon_1 \\ \varepsilon_2 \\ \vdots \\ \varepsilon_n \end{pmatrix}$$

$\mathbf{X}$ is the **design matrix** — an $n \times (p+1)$ matrix with

a column of ones (for the intercept) and one column per predictor.

::: {.callout-note title="Ordinary Least Squares: deriving the coefficient estimates" collapse="true"}

The goal of OLS is to find the coefficient vector $\hat{\boldsymbol{\beta}}$ that

minimises the **residual sum of squares**:

$$SS_{res} = \sum_{i=1}^n (Y_i - \hat{Y}_i)^2 = (\mathbf{Y} - \mathbf{X}\boldsymbol{\beta})^\top(\mathbf{Y} - \mathbf{X}\boldsymbol{\beta})$$

To minimise, we differentiate with respect to $\boldsymbol{\beta}$ and

set to zero:

$$\frac{\partial SS_{res}}{\partial \boldsymbol{\beta}} = -2\mathbf{X}^\top(\mathbf{Y} - \mathbf{X}\boldsymbol{\beta}) = \mathbf{0}$$

Rearranging gives the **normal equations**:

$$\mathbf{X}^\top\mathbf{X}\hat{\boldsymbol{\beta}} = \mathbf{X}^\top\mathbf{Y}$$

Provided $\mathbf{X}^\top\mathbf{X}$ is invertible (i.e., the predictors

are not perfectly collinear), the unique solution is:

$$\hat{\boldsymbol{\beta}} = (\mathbf{X}^\top\mathbf{X})^{-1}\mathbf{X}^\top\mathbf{Y}$$

This is the **OLS estimator**. It is the Best Linear Unbiased Estimator

(BLUE) under the Gauss-Markov assumptions — it has the smallest

variance of any linear unbiased estimator.

The **fitted values** are:

$$\hat{\mathbf{Y}} = \mathbf{X}\hat{\boldsymbol{\beta}} = \mathbf{X}(\mathbf{X}^\top\mathbf{X})^{-1}\mathbf{X}^\top\mathbf{Y} = \mathbf{H}\mathbf{Y}$$

where $\mathbf{H} = \mathbf{X}(\mathbf{X}^\top\mathbf{X})^{-1}\mathbf{X}^\top$ is

called the **hat matrix** (it puts the "hat" on $\mathbf{Y}$). The

diagonal elements $h_{ii}$ measure the **leverage** of each observation

— how much influence it has on its own fitted value. We return to this

in the diagnostics section.

The **residuals** are:

$$\mathbf{e} = \mathbf{Y} - \hat{\mathbf{Y}} = (\mathbf{I} - \mathbf{H})\mathbf{Y}$$

The variance of the coefficient estimates is:

$$\text{Var}(\hat{\boldsymbol{\beta}}) = \sigma^2 (\mathbf{X}^\top\mathbf{X})^{-1}$$

Since $\sigma^2$ is unknown, we estimate it with the **mean squared

error**:

$$\hat{\sigma}^2 = MSE = \frac{SS_{res}}{n - p - 1}$$

where $n - p - 1$ is the degrees of freedom (sample size minus the

number of estimated parameters). The square root $\hat{\sigma} =

\sqrt{MSE}$ is the **residual standard error** reported by R's

`summary()`.

:::

## Model Assumptions

The standard assumptions are worth keeping in view because almost all of

the diagnostics later in the notebook are checking one of them.

### Linearity

The relationship between each predictor and the outcome is linear in

the parameters. This is checked graphically (scatter plots with LOESS

smoothers, residuals vs fitted plot).

### Independence

Observations are independent of each other. This is violated by

clustered data (e.g., patients within hospitals), repeated measures, or

time series. Violations require mixed effects models, GEE, or time

series methods.

::: {.callout-note title="Survey data and independence" collapse="true"}

NHANES uses a **complex survey design** — a stratified, multistage

probability sample. Participants within the same primary sampling unit

(PSU) may be more similar to each other than to participants from

different PSUs, violating the independence assumption.

A fully correct analysis would use survey-weighted regression via

`survey::svyglm()`, incorporating the sampling weights (`mec_weight`),

PSU (`psu`), and strata (`strata`) variables. This adjusts both

coefficient estimates and standard errors.

For simplicity and pedagogical clarity, this notebook uses unweighted

OLS. The regression notebook in this project uses the same approach.

The substantive findings are unlikely to change dramatically, but

standard errors may be slightly underestimated.

:::

### Normality of Residuals

The residuals $\varepsilon_i$ are normally distributed. This assumption

is needed for valid inference (t-tests and F-tests on coefficients).

With large samples, the central limit theorem means that

non-normality has little practical impact on p-values — but it can

affect prediction intervals.

### Equal Variance (Homoscedasticity)

The variance of the residuals is constant across all fitted values:

$\text{Var}(\varepsilon_i) = \sigma^2$ for all $i$. When this fails

(**heteroscedasticity**), OLS estimates remain unbiased but standard

errors are incorrect — leading to invalid inference.

::: {.callout-note title="What to do when assumptions are violated" collapse="true"}

| Violated assumption | Consequence | Remedies |

|---|---|---|

| **Non-linearity** | Biased coefficients, poor fit | Transform predictor, add polynomial term, use spline |

| **Non-independence** | Underestimated SEs, anti-conservative p-values | Mixed effects model, GEE, cluster-robust SEs |

| **Non-normality** | Invalid inference in small samples | Log-transform outcome, use robust regression |

| **Heteroscedasticity** | Biased SEs, invalid inference | Heteroscedasticity-robust SEs (`vcovHC`), weighted least squares, transform outcome |

In large samples ($n > 500$), mild violations of normality and

homoscedasticity rarely have a meaningful impact on inference. The

independence assumption is the one that tends to matter most regardless

of sample size.

:::

## Categorical Predictors and Dummy Coding

Categorical variables cannot enter a regression model directly — they

must be represented as a set of **dummy (indicator) variables**.

For a categorical variable with $k$ levels, R creates $k - 1$ dummy

variables. Each dummy compares one level to the **reference group**

(the omitted category). For example, with race coded as:

| Variable | Meaning |

|---|---|

| `raceMexican American` | 1 if Mexican American, 0 otherwise |

| `raceOther Hispanic` | 1 if Other Hispanic, 0 otherwise |

| `raceNon-Hispanic Black` | 1 if Non-Hispanic Black, 0 otherwise |

| `raceNon-Hispanic Asian` | 1 if Non-Hispanic Asian, 0 otherwise |

| `raceOther/Multiracial` | 1 if Other/Multiracial, 0 otherwise |

The **reference group** is Non-Hispanic White — the level not

represented by any dummy. Its effect is absorbed into the intercept.

Each coefficient for race represents the **difference in mean SBP

between that group and Non-Hispanic White**, holding all other

predictors constant.

::: {.callout-note title="Why $k - 1$ dummies and not $k$?" collapse="true"}

If we created a dummy variable for every level of a categorical

variable, the columns of the design matrix $\mathbf{X}$ would be

perfectly collinear — they would sum to 1 (the intercept column) for

every row. This is called **perfect multicollinearity**, and it makes

$\mathbf{X}^\top\mathbf{X}$ singular (non-invertible), so the OLS

estimator $(\mathbf{X}^\top\mathbf{X})^{-1}$ does not exist.

The fix is to drop one level — the reference group — so that the

remaining dummies are not a linear combination of each other or of the

intercept.

The choice of reference group does not affect model fit, predicted

values, or the overall F-test. It only affects the interpretation of

the individual dummy coefficients — each is now relative to the chosen

reference.

In R, the reference level is set by factor ordering. The first level

of the factor becomes the reference. We can change this with

`relevel(factor_var, ref = "new_reference")`.

:::

---

# Model Building

## Base Model

We start with a simple demographic model. That gives us a baseline

before adding the social and lifestyle predictors.

```{r}

#| label: model-base

model_base <- lm(sbp ~ age + sex + race, data = df_cc)

summary(model_base)

```

::: {.callout-note title="Reading the R summary output" collapse="true"}

The `summary()` output for an `lm` object contains several key

components:

**Residuals**

A five-number summary of the raw residuals. If the model fits well and

residuals are symmetric, the min/max should be roughly equal in

magnitude, and the median should be close to zero.

**Coefficients table**

| Column | Meaning |

|---|---|

| `Estimate` | The estimated coefficient $\hat{\beta}_j$ |

| `Std. Error` | The standard error $SE(\hat{\beta}_j) = \sqrt{\hat{\sigma}^2 [(\mathbf{X}^\top\mathbf{X})^{-1}]_{jj}}$ |

| `t value` | The test statistic $t = \hat{\beta}_j / SE(\hat{\beta}_j)$, used to test $H_0: \beta_j = 0$ |

| `Pr(>|t|)` | Two-tailed p-value from the t-distribution with $n - p - 1$ degrees of freedom |

**Residual standard error**

$\hat{\sigma} = \sqrt{MSE}$ — the estimated standard deviation of the

residuals. Smaller values indicate better fit. The degrees of freedom

shown ($n - p - 1$) confirm how many parameters were estimated.

**R-squared**

The proportion of variance in $Y$ explained by the model (see Section 6).

**F-statistic**

Tests whether the model as a whole explains significantly more variance

than an intercept-only model. The associated p-value tests $H_0: \beta_1

= \beta_2 = \cdots = \beta_p = 0$.

:::

## Full Model

The full model adds the social and lifestyle variables used throughout

the project.

```{r}

#| label: model-full

model_full <- lm(

sbp ~ age + sex + race +

log_total_met + sedentary_min_day +

waist_cm + education + poverty_ratio +

sleep_hours + smoking_status +

food_security + diabetes_flag,

data = df_cc

)

summary(model_full)

```

::: {.callout-note title="Why build models incrementally?" collapse="true"}

Fitting the base model before the full model is not just convention —

it serves several purposes:

**1. Establishes a baseline for comparison.**

Without a reference point, we cannot quantify what the additional

predictors add. The nested model comparison (Section 6) is only

possible because we have both models.

**2. Reveals confounding.**

If a coefficient changes substantially when we add predictors, it

suggests the original association was confounded. For example, if the

age coefficient changed after adding smoking status, it would suggest

the two are correlated and that the crude age effect was partly

reflecting the older age profile of smokers (or vice versa).

**3. Supports a clear narrative.**

"Demographics alone explain X%; adding social factors explains Y%"

is a more compelling and interpretable finding than presenting a single

full model in isolation.

**4. Parsimony.**

Not all variables need to be in the final model. A model with fewer

predictors that fits nearly as well is preferable — it is more

interpretable, less prone to overfitting, and more robust to new data.

:::

---

# Nested Model Comparison

## Sums of Squares

To compare the base and full models, we need a compact way to describe

fit and improvement.

$$SS_{tot} = SS_{reg} + SS_{res}$$

$$\underbrace{\sum_{i=1}^n (Y_i - \bar{Y})^2}_{SS_{tot}} = \underbrace{\sum_{i=1}^n (\hat{Y}_i - \bar{Y})^2}_{SS_{reg}} + \underbrace{\sum_{i=1}^n (Y_i - \hat{Y}_i)^2}_{SS_{res}}$$

where:

- $SS_{tot}$ (total sum of squares) — total variability in $Y$ around

its mean

- $SS_{reg}$ (regression sum of squares) — variability explained by the

model

- $SS_{res}$ (residual sum of squares) — variability not explained by

the model (unexplained error)

## R-Squared

**R-squared** ($R^2$) is the proportion of total variance explained by

the model:

$$R^2 = \frac{SS_{reg}}{SS_{tot}} = 1 - \frac{SS_{res}}{SS_{tot}}$$

$R^2 \in [0, 1]$, where 0 means the model explains nothing and 1 means

perfect fit.

::: {.callout-warning title="A critical limitation of R²" collapse="true"}

$R^2$ **never decreases** when you add a predictor to the model, even

if that predictor is pure noise. This is because any additional

predictor will absorb at least some residual variance by chance.

This makes $R^2$ a poor criterion for model comparison when models

differ in the number of predictors.

**Adjusted R²** penalises for the number of predictors:

$$\bar{R}^2 = 1 - \frac{SS_{res}/(n - p - 1)}{SS_{tot}/(n - 1)} = 1 - (1 - R^2)\frac{n-1}{n-p-1}$$

Adjusted $R^2$ **can decrease** when a predictor adds less explanatory

power than would be expected by chance. It is a better measure of

model quality when comparing models with different numbers of

predictors.

Neither $R^2$ nor adjusted $R^2$ tells you whether the model is

correctly specified — a high $R^2$ with systematically curved

residuals still indicates a bad model.

:::

## The F-Test for Nested Model Comparison

The formal comparison is an **extra sum of squares F-test**. In plain

terms, it asks whether the extra predictors in the full model reduce the

remaining error enough to matter beyond chance.

Let the **reduced model** (base) have $p_R$ predictors and residual sum

of squares $SS_{res,R}$, and the **full model** have $p_F > p_R$

predictors and $SS_{res,F}$. The number of additional parameters is $q

= p_F - p_R$.

The F-statistic is:

$$F = \frac{(SS_{res,R} - SS_{res,F})\, /\, q}{SS_{res,F}\, /\, (n - p_F - 1)}$$

Under $H_0$ (the additional predictors have no effect), this statistic

follows an $F(q,\, n - p_F - 1)$ distribution. A large F (and small

p-value) indicates the additional predictors jointly explain a

statistically significant amount of additional variance.

::: {.callout-note title="Intuition behind the F-statistic" collapse="true"}

The numerator of the F-statistic measures how much the residual sum of

squares **decreases** when we add the extra $q$ predictors, divided by

$q$ (to get an average improvement per predictor).

The denominator is the residual mean squared error of the full model —

a measure of the noise floor.

If the ratio is large, the additional predictors are reducing

unexplained variance meaningfully relative to the background noise. If

the ratio is close to 1, the gain in explained variance is no more than

we would expect by chance.

The $F(q, n - p_F - 1)$ distribution provides the reference: if $H_0$

is true, what values of $F$ are plausible? A p-value is then the

probability of observing an $F$ as large as or larger than the observed

value under $H_0$.

:::

```{r}

#| label: model-comparison

anova(model_base, model_full)

```

::: {.callout-note title="How to report a nested model comparison" collapse="true"}

A complete report of the model comparison should include:

1. The R² of both models

2. The change in R² ($\Delta R^2$)

3. The F-statistic with its degrees of freedom

4. The associated p-value

**Example reporting:**

> The full model (including social determinants and lifestyle variables)

> explained 17.45% of the variance in SBP ($R^2 = 0.175$), compared to

> 16.54% for the base demographic model ($R^2 = 0.165$). The additional

> predictors jointly explained a statistically significant increment of

> variance ($\Delta R^2 = 0.009$, $F(15, 4853) = 3.59$, $p < 0.001$).

Note the distinction between **statistical significance** and **practical

significance**. A $\Delta R^2$ of 0.009 is real — the F-test confirms

it is unlikely to be due to chance — but it is small. In a clinical

context, a model that explains 17.45% of SBP variance rather than

16.54% does not represent a meaningful improvement in prediction.

**What counts as a meaningful $R^2$?** There is no universal threshold.

In social science and epidemiology, models explaining 10–30% of variance

are common for complex behaviours and outcomes with many unmeasured

drivers. In controlled laboratory settings, $R^2 > 0.90$ is routine. The

appropriate benchmark depends on the discipline and the nature of the

outcome.

:::

```{r}

#| label: r2-table

tibble(

Model = c("Base (age + sex + race)", "Full (+ SDoH & lifestyle)"),

R2 = c(summary(model_base)$r.squared, summary(model_full)$r.squared),

Adj_R2 = c(summary(model_base)$adj.r.squared, summary(model_full)$adj.r.squared),

Sigma = c(summary(model_base)$sigma, summary(model_full)$sigma)

) |>

mutate(across(c(R2, Adj_R2), ~ round(., 4)),

Sigma = round(Sigma, 3)) |>

knitr::kable(

col.names = c("Model", "R²", "Adjusted R²", "Residual SE"),

caption = "Model comparison: variance explained"

)

```

---

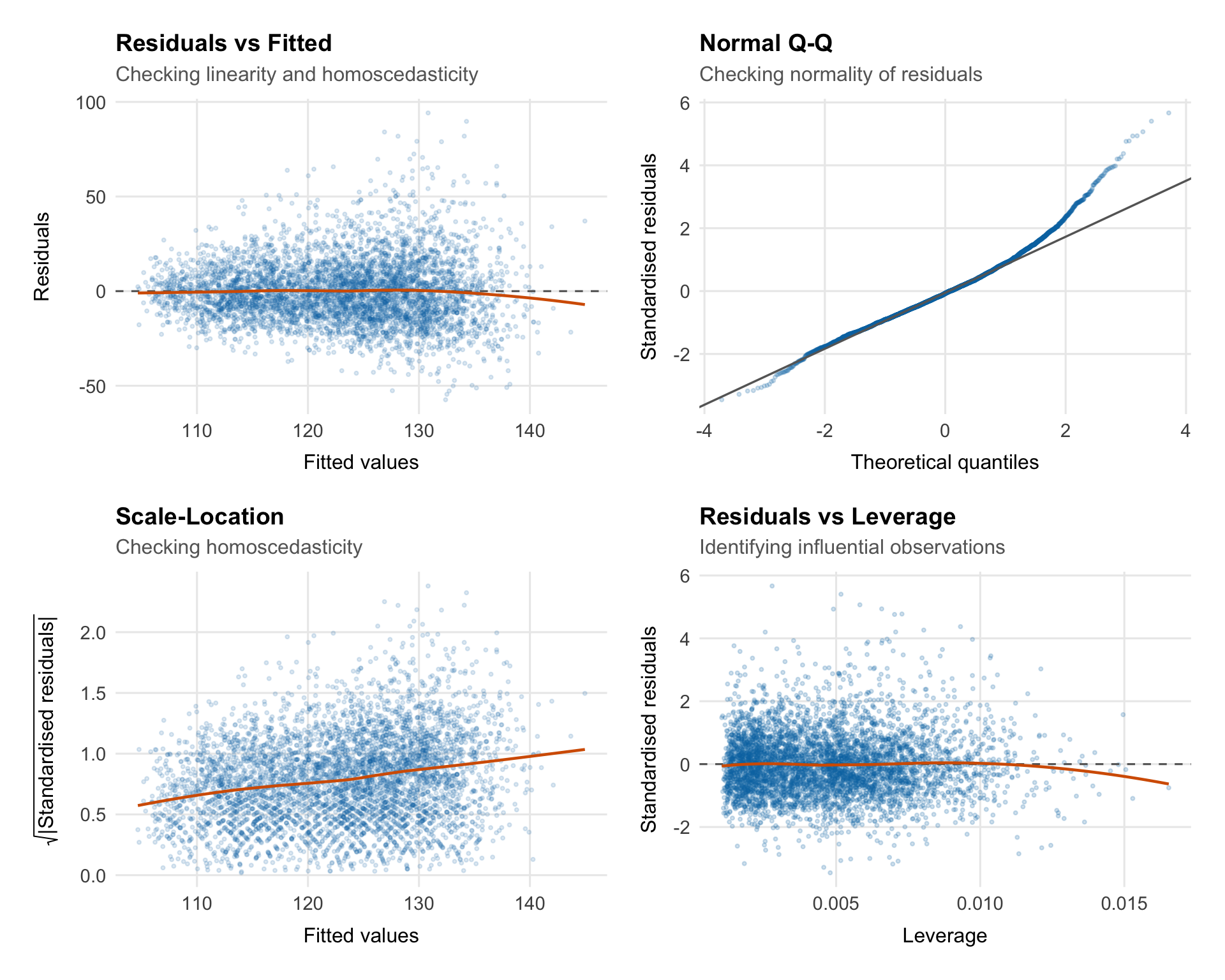

# Model Diagnostics

Fitting the model is only the start. Before interpreting coefficients or

p-values, we need to see whether the residuals look consistent with the

assumptions of ordinary least squares.

## What Are Residuals?

For each observation $i$, the **raw residual** is the difference

between the observed and fitted value:

$$e_i = Y_i - \hat{Y}_i$$

Residuals are the part of SBP the model leaves unexplained. If the model

is behaving reasonably:

- Residuals should be centred around zero

- Residuals should have constant variance across fitted values

- Residuals should be approximately normally distributed

- Residuals should be independent (no patterns over time or across groups)

We use several diagnostic plots to check these properties.

::: {.callout-note title="Raw vs standardised vs studentised residuals" collapse="true"}

**Raw residuals** $e_i = Y_i - \hat{Y}_i$ are on the scale of the

outcome and have unequal variances — observations with high leverage

tend to have smaller residuals because the model is pulled toward them.

**Standardised residuals** divide by an estimate of the residual

standard deviation:

$$r_i = \frac{e_i}{\hat{\sigma}\sqrt{1 - h_{ii}}}$$

where $h_{ii}$ is the leverage of observation $i$ (the $i$-th diagonal

element of the hat matrix $\mathbf{H}$). Standardised residuals should

be approximately $N(0, 1)$, so values beyond $\pm 2$ or $\pm 3$ suggest

potential outliers.

**Studentised (externally studentised) residuals** go one step further

— they refit the model without observation $i$ and use that model's

$\hat{\sigma}_{-i}$ to standardise:

$$t_i = \frac{e_i}{\hat{\sigma}_{-i}\sqrt{1 - h_{ii}}}$$

These follow a $t_{n-p-2}$ distribution and are more sensitive to

outliers. R's `rstudent()` function returns these.

:::

## Diagnostic Plots

```{r}

#| label: fig-diagnostics

#| fig-width: 10

#| fig-height: 8

aug <- augment(model_full)

p1 <- ggplot(aug, aes(x = .fitted, y = .resid)) +

geom_point(alpha = 0.15, size = 0.7, colour = palette_epi[["blue"]]) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "grey40") +

geom_smooth(method = "loess", se = FALSE, colour = palette_epi[["vermillion"]],

linewidth = 0.8) +

labs(title = "Residuals vs Fitted",

subtitle = "Checking linearity and homoscedasticity",

x = "Fitted values",

y = "Residuals") +

theme_epi(grid = "both")

p2 <- ggplot(aug, aes(sample = .std.resid)) +

stat_qq(alpha = 0.2, size = 0.7, colour = palette_epi[["blue"]]) +

stat_qq_line(colour = "grey40", linewidth = 0.6) +

labs(title = "Normal Q-Q",

subtitle = "Checking normality of residuals",

x = "Theoretical quantiles",

y = "Standardised residuals") +

theme_epi(grid = "both")

p3 <- ggplot(aug, aes(x = .fitted, y = sqrt(abs(.std.resid)))) +

geom_point(alpha = 0.15, size = 0.7, colour = palette_epi[["blue"]]) +

geom_smooth(method = "loess", se = FALSE, colour = palette_epi[["vermillion"]],

linewidth = 0.8) +

labs(title = "Scale-Location",

subtitle = "Checking homoscedasticity",

x = "Fitted values",

y = expression(sqrt("|Standardised residuals|"))) +

theme_epi(grid = "both")

p4 <- ggplot(aug, aes(x = .hat, y = .std.resid)) +

geom_point(alpha = 0.2, size = 0.7, colour = palette_epi[["blue"]]) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "grey40") +

geom_smooth(method = "loess", se = FALSE, colour = palette_epi[["vermillion"]],

linewidth = 0.8) +

labs(title = "Residuals vs Leverage",

subtitle = "Identifying influential observations",

x = "Leverage",

y = "Standardised residuals") +

theme_epi(grid = "both")

(p1 | p2) / (p3 | p4)

```

### Residuals vs Fitted

::: {.callout-note title="What this plot checks — and what to look for" collapse="true"}

**What it checks:** Linearity and homoscedasticity simultaneously.

**The x-axis** shows the fitted values $\hat{Y}_i$ — the model's

predictions. **The y-axis** shows the raw residuals $e_i = Y_i -

\hat{Y}_i$.

**What we want to see:**

- Points scattered randomly around zero with no systematic pattern

- Roughly equal spread across the range of fitted values

- The LOESS smoother (red line) should be approximately flat at zero

**What would concern us:**

- A **curve** in the LOESS smoother suggests non-linearity — some

predictor(s) have a non-linear effect that the model is not capturing

- A **funnel shape** (spread increasing with fitted values) indicates

heteroscedasticity — the variance of errors is not constant

- A **horizontal band** that widens or narrows suggests the same

**What to do if this fails:**

- Non-linearity: add polynomial terms, splines, or transform the

predictor(s)

- Heteroscedasticity: use heteroscedasticity-robust standard errors

(`sandwich::vcovHC()`), weighted least squares, or transform the

outcome

:::

### Normal Q-Q Plot

::: {.callout-note title="What this plot checks — and what to look for" collapse="true"}

**What it checks:** Normality of residuals.

A Q-Q plot compares the **empirical quantiles** of the standardised

residuals against the **theoretical quantiles** of a standard normal

distribution. If the residuals are normally distributed, the points

should fall on the diagonal reference line.

**What we want to see:**

- Points tracking closely along the diagonal line

**What would concern us:**

- **Heavy tails** (points curving away from the line at both ends)

indicate a distribution with more extreme values than the normal

— the model is producing more large residuals than expected

- **Light tails** (points flatter than the line at the ends) indicate

fewer extremes than the normal

- **Systematic curvature** (S-shaped pattern) indicates skewness in the

residuals

**What to do if this fails:**

In large samples ($n > 500$), moderate departures from normality have

little effect on inference — the central limit theorem ensures that

coefficient estimates are approximately normally distributed regardless.

For smaller samples or severe non-normality, consider transforming the

outcome or using bootstrap confidence intervals.

:::

### Scale-Location

::: {.callout-note title="What this plot checks — and what to look for" collapse="true"}

**What it checks:** Homoscedasticity (equal variance).

Also called the **spread-location plot**, this plots $\sqrt{|r_i|}$

(the square root of the absolute standardised residuals) against fitted

values. The square root transformation stabilises the scale and makes

trends in spread easier to detect.

**What we want to see:**

- A roughly horizontal LOESS smoother

- Points scattered evenly across the range of fitted values

**What would concern us:**

- An **upward slope** indicates increasing variance with fitted values

(the most common form of heteroscedasticity)

- A **downward slope** indicates decreasing variance

- Any systematic trend is a problem

**A formal test:** The Breusch-Pagan test (`car::ncvTest()`) provides a

p-value for the null hypothesis of constant variance.

:::

```{r}

#| label: breusch-pagan

car::ncvTest(model_full)

```

### Residuals vs Leverage

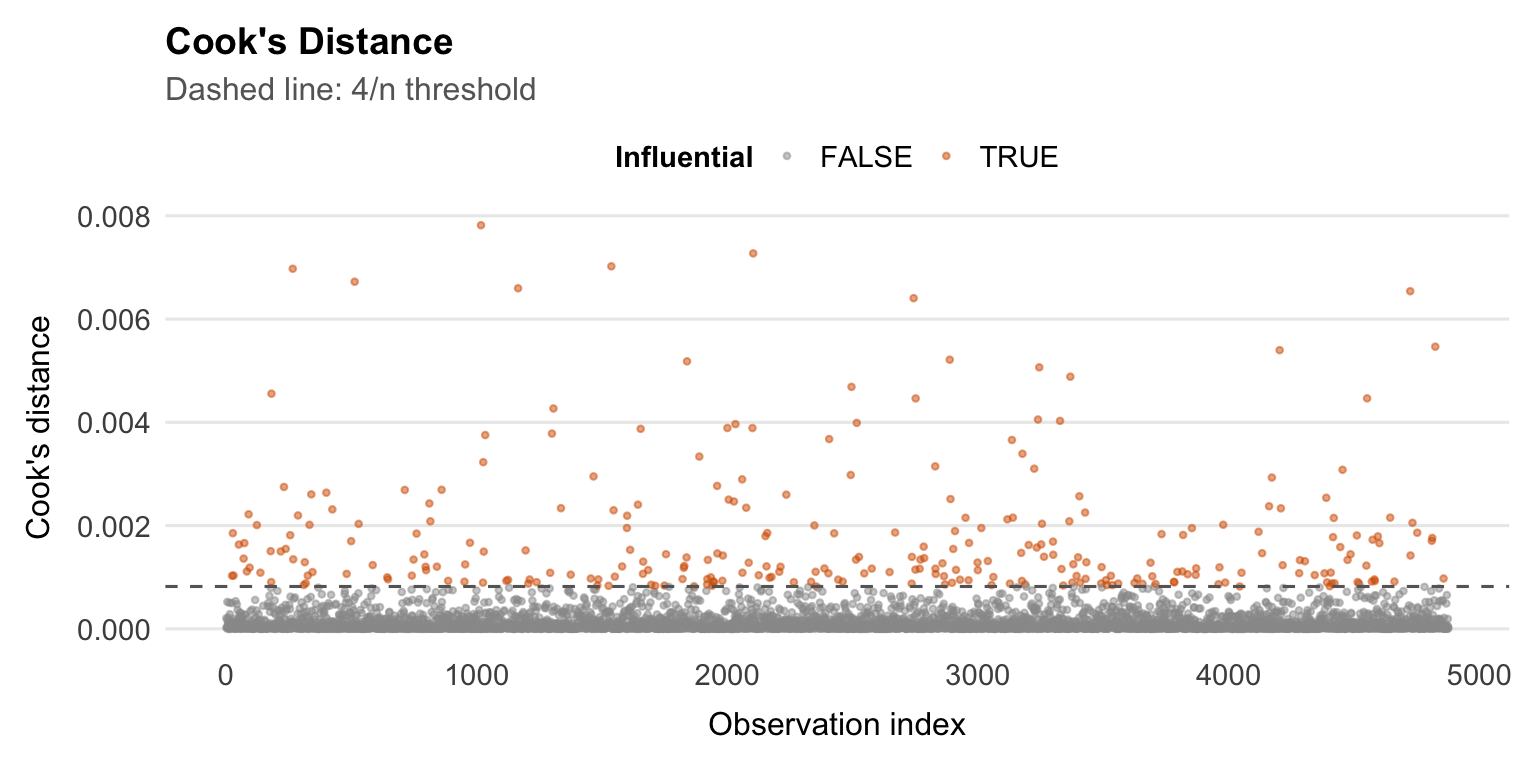

::: {.callout-note title="Leverage, influence, and Cook's Distance" collapse="true"}

**Leverage** measures how unusual an observation's predictor values

are — how far the observation is from the centre of the predictor

space. The leverage of observation $i$ is the $i$-th diagonal element

of the hat matrix:

$$h_{ii} = [\mathbf{H}]_{ii} = [\mathbf{X}(\mathbf{X}^\top\mathbf{X})^{-1}\mathbf{X}^\top]_{ii}$$

$h_{ii}$ ranges from $1/n$ to 1. High leverage observations have

unusual predictor values. They may or may not be **influential** —

that depends on whether their residual is also large.

**Influence** combines leverage and residual size. The most widely used

measure is **Cook's Distance**:

$$D_i = \frac{e_i^2}{(p+1)\, MSE} \cdot \frac{h_{ii}}{(1 - h_{ii})^2}$$

Cook's $D_i$ measures how much the entire vector of fitted values

changes if observation $i$ is removed from the dataset. It combines the

size of the residual (numerator) with the leverage (denominator).

Common rules of thumb:

- $D_i > 1$: potentially influential

- $D_i > 4/n$: a more conservative threshold often used in practice

**The Residuals vs Leverage plot** helps identify observations that are

both high leverage and high residual — the most dangerous combination.

Cook's distance contours are sometimes overlaid (dashed lines) to mark

influential points.

**What to do with influential observations:**

1. Check for data entry errors first

2. Understand *why* they are influential (extreme predictor values?

data quality issues?)

3. Refit the model without them and compare results — if estimates

change substantially, report sensitivity analyses

4. Never remove observations solely because they are influential without

a substantive justification

:::

```{r}

#| label: cooks-distance

#| fig-width: 8

#| fig-height: 4

aug |>

mutate(index = row_number(),

influential = .cooksd > 4 / nrow(df_cc)) |>

ggplot(aes(x = index, y = .cooksd, colour = influential)) +

geom_point(size = 0.8, alpha = 0.5) +

geom_hline(yintercept = 4 / nrow(df_cc), linetype = "dashed",

colour = "grey40") +

scale_colour_manual(values = c("FALSE" = "grey60", "TRUE" = palette_epi[["vermillion"]])) +

labs(

title = "Cook's Distance",

subtitle = "Dashed line: 4/n threshold",

x = "Observation index",

y = "Cook's distance",

colour = "Influential"

) +

theme_epi(grid = "y") +

theme(legend.position = "top")

```

## Variance Inflation Factors

As a final diagnostic, we check for multicollinearity using Variance

Inflation Factors (VIFs).

The VIF for predictor $j$ is:

$$VIF_j = \frac{1}{1 - R_j^2}$$

where $R_j^2$ is the $R^2$ from regressing $X_j$ on all other

predictors. It quantifies how much the variance of $\hat{\beta}_j$ is

inflated by collinearity relative to what it would be if $X_j$ were

uncorrelated with all other predictors.

- $VIF = 1$: no collinearity

- $VIF = 5$: moderate collinearity ($SE$ inflated by $\sqrt{5} \approx 2.2$)

- $VIF = 10$: high collinearity (commonly used as a threshold for concern)

```{r}

#| label: vif

car::vif(model_full)

```

::: {.callout-note title="Interpreting VIF output for categorical variables" collapse="true"}

For categorical predictors with more than two levels, `car::vif()`

returns a **Generalised VIF (GVIF)** rather than a standard VIF. The

GVIF accounts for the fact that a multi-level factor is represented by

multiple dummy variables.

To compare GVIFs across predictors with different numbers of

parameters, the adjusted value $GVIF^{1/(2 \cdot df)}$ is reported —

where $df$ is the number of degrees of freedom for that term (i.e., the

number of dummy variables). This is equivalent to the square root of

the VIF for binary predictors.

A rule of thumb: $GVIF^{1/(2 \cdot df)} > \sqrt{10} \approx 3.16$

flags a potential collinearity problem, consistent with the $VIF > 10$

threshold for continuous predictors.

:::

---

# Interpreting Coefficients

## Continuous Predictors

For a continuous predictor $X_j$, the coefficient $\hat{\beta}_j$

represents the estimated change in mean SBP for a one-unit increase in

$X_j$, with the other predictors held fixed.

For example, for age:

> "Each additional year of age is associated with a

> `r round(coef(model_full)["age"], 2)` mmHg increase in SBP, after

> adjusting for sex, race, and all social and lifestyle predictors."

That "holding all other predictors constant" language matters. These are

partial associations inside a multivariable model, not standalone or

causal effects.

## Categorical Predictors

For a categorical predictor, each coefficient is the adjusted mean

difference in SBP between that level and the reference group.

For education, with "College graduate or above" as the reference:

> "Participants with less than a 9th grade education had SBP

> `r round(coef(model_full)["educationLess than 9th grade"], 2)` mmHg

> higher than college graduates, on average, after adjusting for all

> other variables in the model."

## Log-Transformed Predictors

When a predictor is log-transformed, the raw coefficient is harder to

read directly because a one-unit increase in $\log(X)$ corresponds to

multiplying $X$ by about 2.7.

More useful interpretations:

**A doubling of $X$:**

$$\Delta Y = \hat{\beta}_j \times \log(2) \approx 0.693 \times \hat{\beta}_j$$

**A 10% increase in $X$:**

$$\Delta Y \approx \hat{\beta}_j \times \log(1.10) \approx 0.095 \times \hat{\beta}_j$$

For our physical activity variable (`log_total_met`):

> "A doubling of total physical activity (in MET-minutes per week) is

> associated with a

> `r round(coef(model_full)["log_total_met"] * log(2), 2)` mmHg change

> in SBP, after adjustment."

::: {.callout-note title="Reporting coefficients vs p-values" collapse="true"}

A common but problematic habit is to report only whether a coefficient

is "significant" (p < 0.05) rather than the estimated magnitude and

its uncertainty. Statistical significance tells you that the estimate is

unlikely to be zero by chance — it says nothing about whether the effect

is large enough to matter in practice.

**Best practice is to report:**

1. The coefficient estimate $\hat{\beta}$ (the magnitude of the effect)

2. The 95% confidence interval (the uncertainty around the estimate)

3. The p-value (the strength of evidence against the null)

For example:

| Predictor | $\hat{\beta}$ (mmHg) | 95% CI | p-value |

|---|---|---|---|

| Age (per year) | +0.40 | (0.37, 0.43) | < 0.001 |

| Non-Hispanic Black vs White | +4.93 | (3.87, 5.99) | < 0.001 |

| < 9th grade vs college grad | +5.40 | (3.21, 7.59) | < 0.001 |

This makes clear that while all three are statistically significant,

the racial disparity and education effect are of comparable magnitude,

while the age effect per year is small (though cumulative over decades

it is substantial).

Reporting only stars (***, **, *) discards the magnitude and direction

of the effect entirely — always report the number.

:::

```{r}

#| label: tbl-coefficients

tidy(model_full, conf.int = TRUE) |>

filter(term != "(Intercept)") |>

mutate(

term = str_remove(term, "^(race|education|smoking_status|food_security|sex|diabetes_flag)"),

across(c(estimate, conf.low, conf.high), ~ round(., 2)),

p.value = case_when(

p.value < 0.001 ~ "< 0.001",

p.value < 0.01 ~ "< 0.01",

p.value < 0.05 ~ paste0(round(p.value, 3)),

TRUE ~ paste0(round(p.value, 2))

),

ci = paste0("(", conf.low, ", ", conf.high, ")")

) |>

select(term, estimate, ci, p.value) |>

knitr::kable(

col.names = c("Predictor", "β (mmHg)", "95% CI", "p-value"),

caption = "Full model: adjusted coefficient estimates"

)

```

---

# Limitations and Caveats

The results are useful, but they have clear limits:

**Cross-sectional design.** NHANES captures a snapshot in time. We

observe associations between SBP and social factors at one point, but

cannot infer that changes in social factors would cause changes in SBP.

Longitudinal data would be needed to make causal claims.

**Missing variables.** The most likely explanation for the model's

modest $R^2$ is unmeasured variables — particularly **antihypertensive

medication use**. Participants taking blood pressure medication will

have artificially suppressed SBP relative to their "true" underlying

level. Without controlling for this, the effects of social factors are

attenuated and their relationship to SBP is distorted.

**Complete case analysis.** Restricting to participants with non-missing

data on all variables may introduce selection bias if missingness is

related to SBP or social factors. Multiple imputation would address

this but was not used here.

**Survey design.** NHANES uses a complex stratified sampling design.

Unweighted OLS does not account for sampling weights, PSUs, or strata.

The coefficient estimates may be approximately unbiased, but standard

errors and confidence intervals may be slightly underestimated.

**Residual confounding.** Even after adjusting for 12 predictors, there

will be unmeasured variables correlated with both the social factors and

SBP. The observed associations — particularly the racial disparity —

should not be interpreted as the total causal effect.